With zonal pricing now ruled out by the Secretary of State, Regen director Johnny Gowdy considers the challenges and opportunities still facing the government – and argues that a far-reaching programme of progressive market reform is urgently needed to deliver investment and meaningful benefits for consumers before the next election. This will require leadership and clear accountability from UK energy policymakers, and for the industry to get behind the reform agenda.

After three years of sometimes-fraught debate and consultation, we are pleased that a decision on zonal pricing has now been made, removing a critical barrier to unlock the billions of pounds of investment needed to decarbonise the GB power sector.

The wide range of perspectives shared throughout this debate has highlighted that reform and innovation are urgently needed to tackle underlying inefficiencies and costs in the energy market and the operation of the wider energy system. This will require strong leadership from the UK government and a very clear set of accountabilities for the regulator and system operator. It will also require the industry to get behind the reform agenda and work constructively towards a common goal, as has happened in grid connection reform. Regen looks forward to supporting that endeavour.

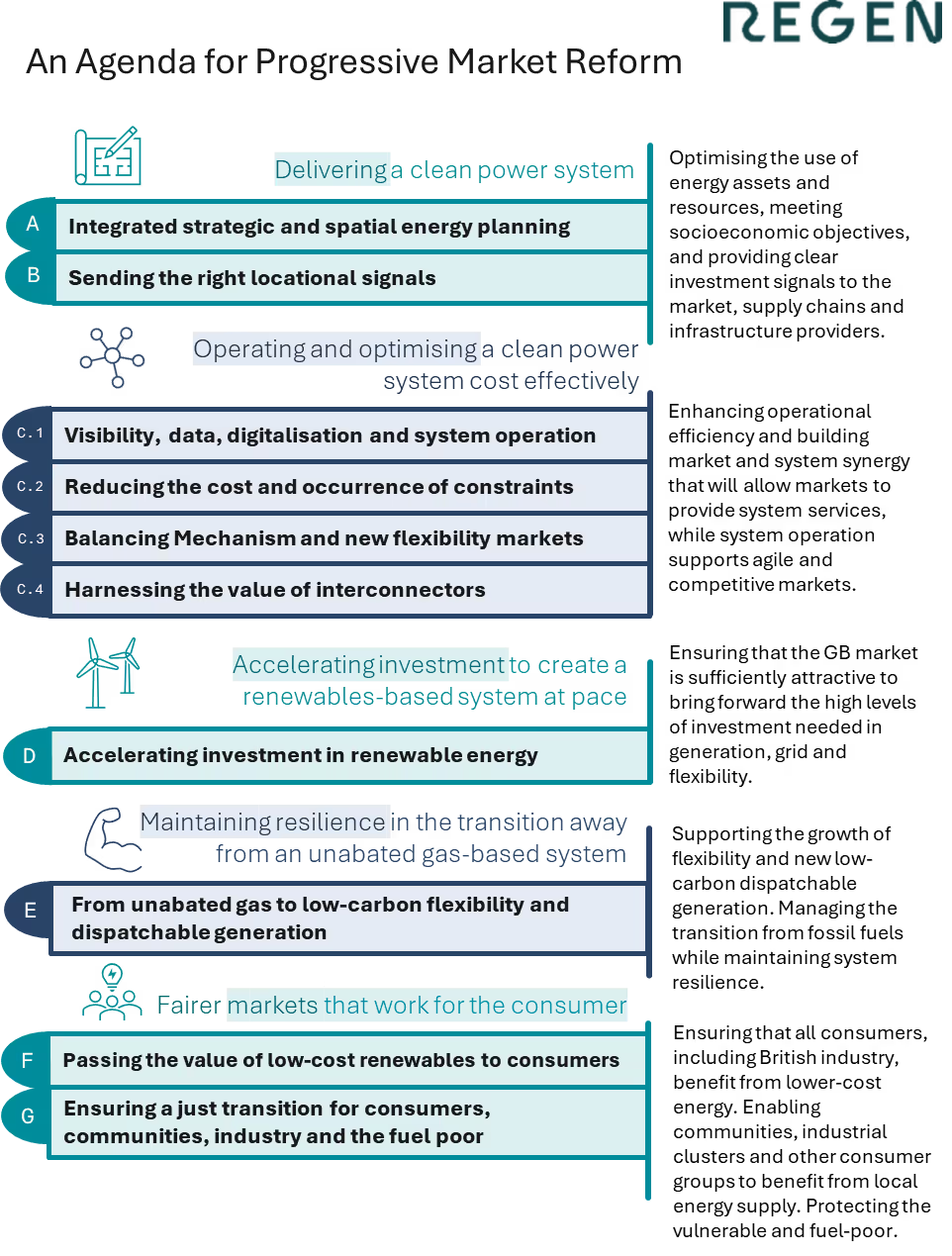

Regen’s 2024 paper An Agenda for Progressive Market Reform set out our thinking on a far-reaching agenda for market, investment policy and operational reform within a national market.

There are many areas of reform needed but, critically, we need to find ways to reduce both the occurrence and the cost of managing network constraints, which have risen to over £1.7 billion in 2024/25 and could, without action, continue to rise into the early 2030s. Regen’s suggested actions to reduce constraint costs are set out below. The first of these is to establish greater accountability and transparency. During the REMA debate, perhaps because constraints were the main driver of zonal benefits, alternative constraint management proposals gained little traction.

Other areas where we would like to see greater focus include the future of the Contract for Difference scheme, the Capacity Market, network charging, competition in both the wholesale and retail markets, expansion of the balancing mechanism, community co-ownership and local energy supply. The Industrial Strategy also rightly highlighted the expansion of the forward market for corporate Power Purchase Agreements (cPPAs) as key opportunity for energy cost reduction.

None of these reforms will be easy to implement or will happen overnight, but they are practical objectives that could be delivered in this Parliament and will help to reduce consumer bills before the next election.

The strength of debate on market reform has demonstrated the level of passion in the energy sector to achieve a clean, affordable and reliable power system. It will now be vital for the industry and policymakers to work together to harness that passion, build trust and show that we can deliver meaningful benefits for the UK consumer. Time is of the essence.

Regen's constraint cost reduction proposals

Constraint cost reduction will require focus and commitment on the part of networks, policymakers and regulators. Regen’s view is that this will include:

Ensuring clear accountability and responsibility for constraint cost reduction between NESO, network operators and Ofgem. We must stop treating constraints as an inevitable “pass-through” cost for consumers.

Accelerating network investment to catch up after a decade of delayed grid projects, delivering on the ASTI and Electricity Networks Commissioner reforms.

Aligning future network build and clean power plans, including proactive connection queue management and network charging reforms

Targeted use of risk-sharing ‘non-firm connections’ that are time-limited and capped to enable earlier and lower cost connections within constraint management areas.

Taking steps to reduce and optimise the occurrence of network outages, which have become the key driver for higher constraints across transmission boundaries. This must include stronger incentives for network operators and NESO to consider the whole system costs of outages.

Opening up the Balancing Mechanism to increased competition from storage and demand-side response to reduce reliance on higher-cost gas generation.

Continued improvement to the NESO control room dispatch capability and IT system to reduce ‘skip rates’ and lower the cost of balancing actions.

Using AI and digitalisation to reduce outages and greatly improve constraint and grid capacity forecasting.

Technical solutions to maximise grid availability, including the expansion of dynamic line management, inter-trip services, AI-backed monitoring and active network management.

Creation of local constraint markets and procurement of competitive flexibility services.

A review of regulatory rules to ensure that storage and flexibility assets within constrained areas support system actions, and do not add to constraint costs.

Increased coordination and cooperation between GB and EU system operators, building on wider GB/EU trade agreements, to reduce the cost of managing interconnector flows to alleviate GB constraints, including SO-SO trading arrangements, capacity allocation and integrated balancing.