The recent Contracts for Difference (CfD) Allocation Round 5 (AR5) flop for fixed offshore wind has made headlines, but the auction impacts for floating offshore wind (FLOW) and tidal stream technologies were just as dramatic. Becky Fowell, Energy Analyst, explores what the results mean for these technologies.

Since the release of the AR5 Contracts for Difference (CfD) results, the focus has been on the obvious lack of bids from fixed offshore wind projects. By now, the factors behind this are common knowledge: an increase in supply chain costs, a jump in interest rates and competition for international capital were simply incompatible with the low administrative strike price (ASP) of £44/MWh set by the government for offshore wind.1

We understand that the government has since been working with offshore wind developers to rectify matters to prevent déjà vu in future rounds. In the coming months, we may see new higher ASPs announced for the next round of CfD auctions, AR6.

Media coverage has understandably focused on the hugely disappointing outcome for fixed offshore wind projects due to the immediate risk this poses to the UK's net zero targets, sector jobs and supply chain investment. Less focus has been given to the auction results for the more innovative technologies of tidal and FLOW. These technologies may be small-scale today, but will be critical for the UK's future energy system and create commercial and export opportunities for UK businesses.

In this insight piece, we explore:

Why there were no bids for floating offshore wind projects either

The bespoke support for floating wind that is needed

The AR5 success of tidal stream, as tidal projects pick up the allocation budget left by FLOW

The support needed to build a future pipeline and maintain momentum for both tidal stream and offshore wind

Floating offshore wind - no bids for the innovative technology

Like fixed offshore wind, AR5 was also disappointing for FLOW. This round was expected to see at least three floating wind demonstration projects coming forward and set the benchmark for FLOW costs in the UK.2

Similar cost inflation factors, plus the relatively early stage of technology development for FLOW, meant that the £116/MWh ASP was too low for projects to be viable. As a result, none of the three eligible projects (totalling c.260 MW) put forward a bid, despite all three having secured marine licenses and environmental consent.

This was a frustrating blow for a developing industry in which the UK has ambitions to be a future world leader. In the short term, it is a setback for technology development and innovation. However, if not addressed in future rounds, delays to floating wind development at this early stage will affect the long-term expansion of offshore wind and the UK's future energy security, risking the UK losing momentum and its position as a sector lead.

The negative investment signal of a failed auction round goes beyond the individual project and technology developers. These early-stage projects are intended to kick-start investment in port infrastructure and supply chain capability needed to integrate and deploy FLOW at scale, which is now at risk. This is particularly pertinent to The Crown Estate's upcoming Celtic Sea leasing round, which has now increased to 4.5 GW and is expected to start at the end of 2023.3 Government's refusal to heed the industry's warnings about AR5, plus investment delays in ports and infrastructure, will do little to signal to the market that the UK is ready for floating wind.

Bespoke support for floating wind is needed

The progression of FLOW has been aided by previous development of fixed offshore wind. However, with larger towers and nacelles, first-of-a-kind floating substructures and intricate port logistics, FLOW is very much an innovative technology. Globally, only 121 MW of test and demonstration projects have been consented and built as of 2022.4 In comparison, 13.8 GW of fixed offshore wind has been commissioned in UK waters alone.5

If we are to build 5 GW of floating wind by 2030, the government must recognise the risks and challenges associated with floating wind alongside the opportunity. This can be achieved by allowing industry to learn from the build-out of test and demonstration projects.

Anticipatory investment is critical in kick-starting investment in the industry, facilitating coordination of future projects and signalling the opportunity to the market. In 2014, the FIDER scheme provided investment contracts to some of the first large-scale (>400 MW) fixed offshore wind projects. These initial contracts awarded strike prices of £155/MWh - significantly more than the ASPs for the first pre-commercial (100 MW) floating wind projects. These initial contracts, albeit expensive, triggered investment in fixed offshore wind, and a similar approach is needed for FLOW.

For FLOW, Regen believes that future Allocation Rounds should provide bespoke support through:

Dedicating a pot to floating wind (akin to Pot 3 in AR4) or at least a minimum level of support (such as a ringfence minima)

Increasing the CfD contract length from 15 to 20 years, which developers have told us would help with securing finance

Better accounting for the technology maturity and additional development risk within the ASP.

Any combination of these recommendations would provide greater support for FLOW, a key technology in the UK's future energy mix.

Tidal stream capacity doubles as tidal picks up additional allocation budget left by FLOW

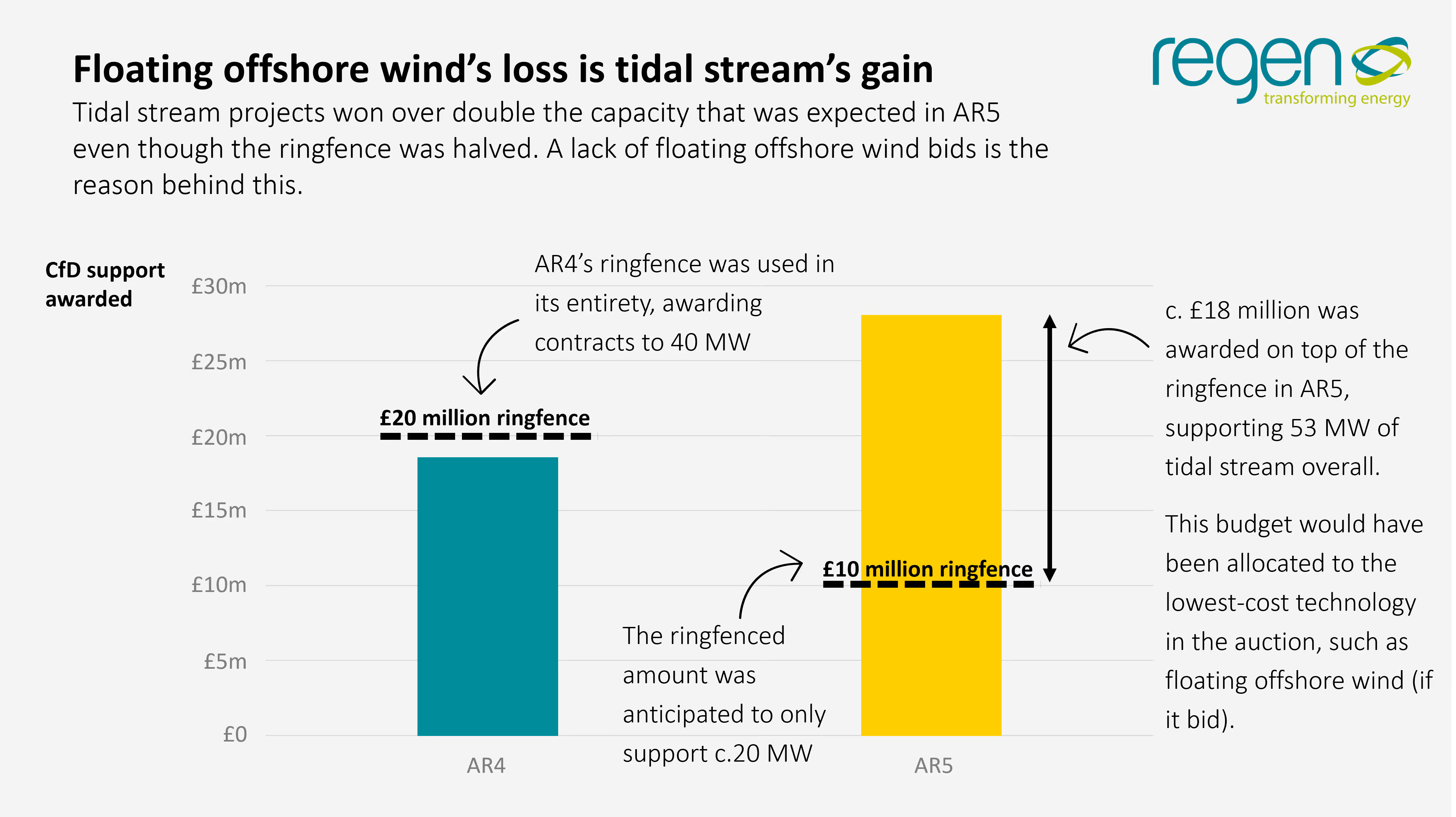

After the success of AR4, expectations for tidal stream were high in AR5. Despite the ringfence minima halving from £20 million to £10 million, 53 MW of tidal stream projects across Wales and Scotland secured contracts at close to the maximum ASP, picking up additional allocation round budget left on the table by FLOW developers.

Established industry players bagged around two-thirds of this capacity, proving that the commercialisation of tidal stream is in progress:

SAE Renewables' Meygen, which has generated over 51 GWh to date and represents c.75% of global tidal stream electricity generation, acquired a further 22 MW of CfD contracts. This means that 60% of its consented pipeline now has financial support.

Orbital Marine Power, which has developed and operated the world's most powerful tidal turbine since 2021, secured CfDs for an additional 7.2 MW capacity, matching its success in AR4.

Both companies have ambitious plans and a combined potential of over 450 MW of tidal stream across the UK, so it is encouraging that further support has been provided.

Magallanes Renovables also received its second batch of CfDs and now holds contracts for 10.1 MW, split across Scotland's EMEC and Wales' Morlais. A further 19 MW of tidal stream support was awarded to Mor Energy, Hydrowing and Verdant Isles - each organisation's first CfD win. The awarding of contracts to new entrants is encouraging growth for the sector and ensuring these first-time contract winners are at the stage where they can bid into future rounds remains the next step.

Support needed to build a future pipeline and maintain momentum

AR5 was an unexpected win for the tidal stream industry, which benefitted from the lack of bids from FLOW. However, as concerns regarding CfD support for FLOW are resolved, future rounds may see less budget available to tidal stream projects, as any budget outside of a ringfence will be awarded to the lower-cost technology (even with the inclusion of non-price factors), which is expected to be FLOW.

Awarding contracts to the lowest-cost technology via the CfD process aims to deliver projects at lowest cost to consumers. However, setting FLOW to compete against tidal stream for auction budget risks the development of both technologies and could hinder the UK's journey to reach net zero.

The build-out of FLOW will be critical in delivering low-cost electricity for UK consumers, and its importance should not be understated. However, both technologies are needed within the future energy system, particularly when considering non-price factors. Tidal stream has significant energy system value as a predictable resource decoupled from other renewable sources. At the same time, FLOW provides geographical diversity to the UK's wind fleet and opens up deeper waters with higher and more consistent wind speeds. Both technologies will also offer the UK significant economic benefits through supply chain, skills and infrastructure development - tidal stream already boasts c.75% UK content in their supply chains, delivering significant economic value to the UK.6

The success of tidal stream in this year's auction demonstrated an appetite to invest in new and innovative technology. It is important that the government continues to nurture tidal stream development and avoids a stop-start cycle of investment, as happened in 2016 when the government abruptly cut revenue support for the marine energy sector. The success of projects and organisations on the cusp of commercialisation is critical to building confidence and momentum in the industry. But equally, ensuring that less-established players are not pressured to reduce costs in lieu of development is just as critical for industry development.

Using the CfD mechanism to support new and mature technologies has always been challenging. There is a way to do this, but it requires careful management to ensure that there is sufficient funding in future allocation rounds, as well as a minimum price set aside for tidal to encourage the development of a longer-term pipeline for commercial scale projects while supporting new technologies to get to demonstration scale. Squeezing the industry too hard in AR6 and beyond will stifle the industry's pipeline of projects, which is vital for progressing towards lower energy costs - particularly for developers who have just won CfD support.

The government needs to decide how best to support the development of both FLOW and tidal stream energy, as both technologies will have a critical role in the UK's future energy system while offering valuable commercial and export opportunities for UK businesses. To realise this, immediate financial support must be aligned with future market signals for both industries. A competitive race to the bottom for two technologies on the cusp of commercialisation is hardly the best mechanism to achieve this.

Endnotes

1 Strike prices shown in 2012 prices. An ASP is an auction reserve or maximum price threshold for bids. If the ASP is too low, projects are not viable and developers do not bid.

2 Twinhub's low bid of £87/MWh in AR4 was supported by the existing consent and grid infrastructure that were acquired from Cornwall Council.