Low auction prices confirm that renewables are cheapest but we could have had a lot more. Now is the time to extend the use of Contracts for Difference to create a new deal between low carbon generators and the UK consumer.

Low auction prices confirm that renewables are cheapest but we could have had a lot more. Now is the time to extend the use of Contracts for Difference to create a new deal between low carbon generators and the UK consumer.

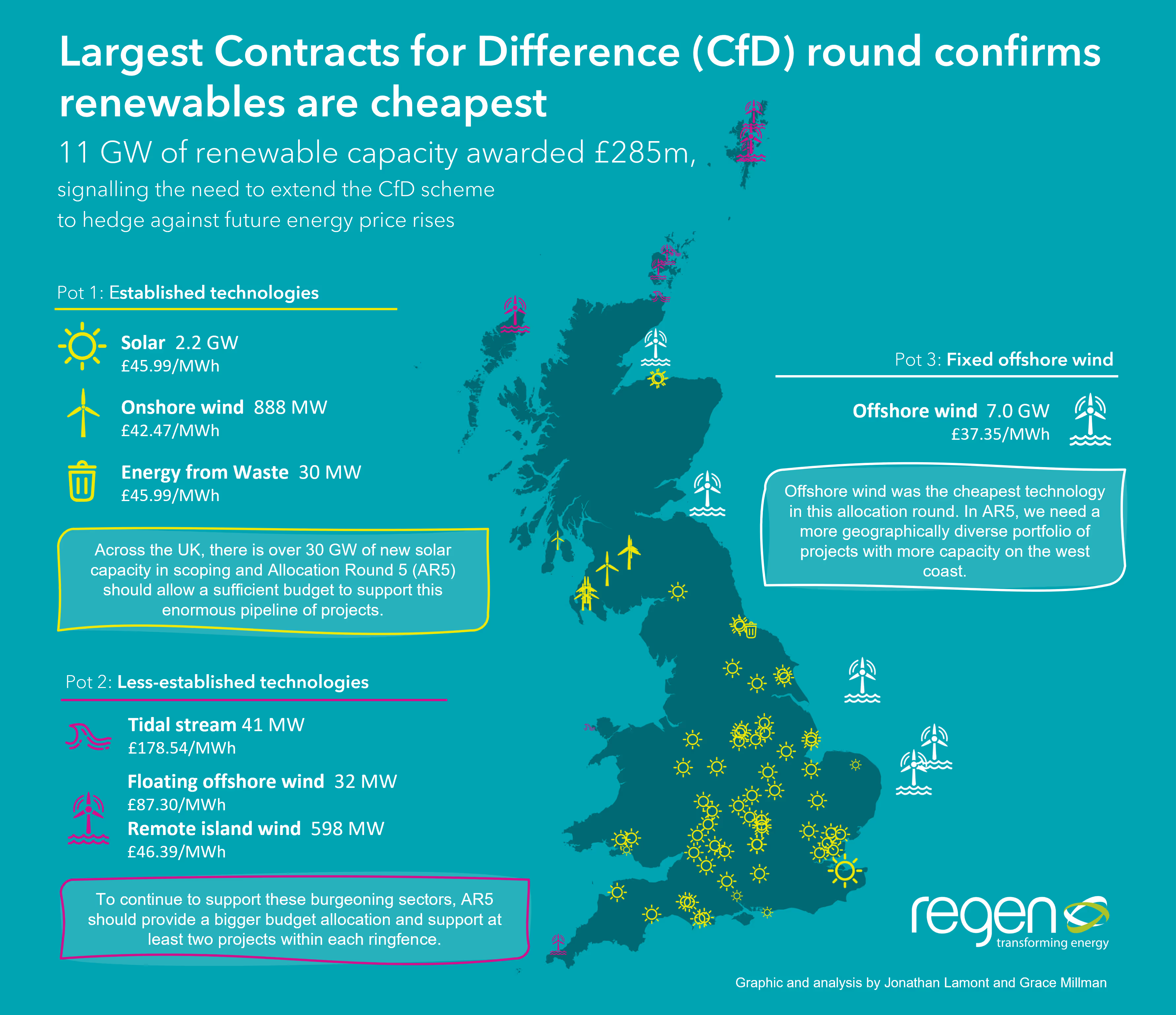

The Contract for Difference (CfD) Allocation Round 4 (AR4) results are out and, once again, renewables have come in with very low strike prices. As most policy makers are now aware, a low strike price means that at times of high market prices, like today, CfD contract holders will be making net payments back into the levy scheme to reduce consumer bills. Regen has been arguing for some time that the UK government should expand the CfD scheme, both in terms of its scope and timing, and make a much larger commitment to renewable energy deployment. This would help to deliver net zero and make a substantial hedge for the UK consumer against future energy price rises.

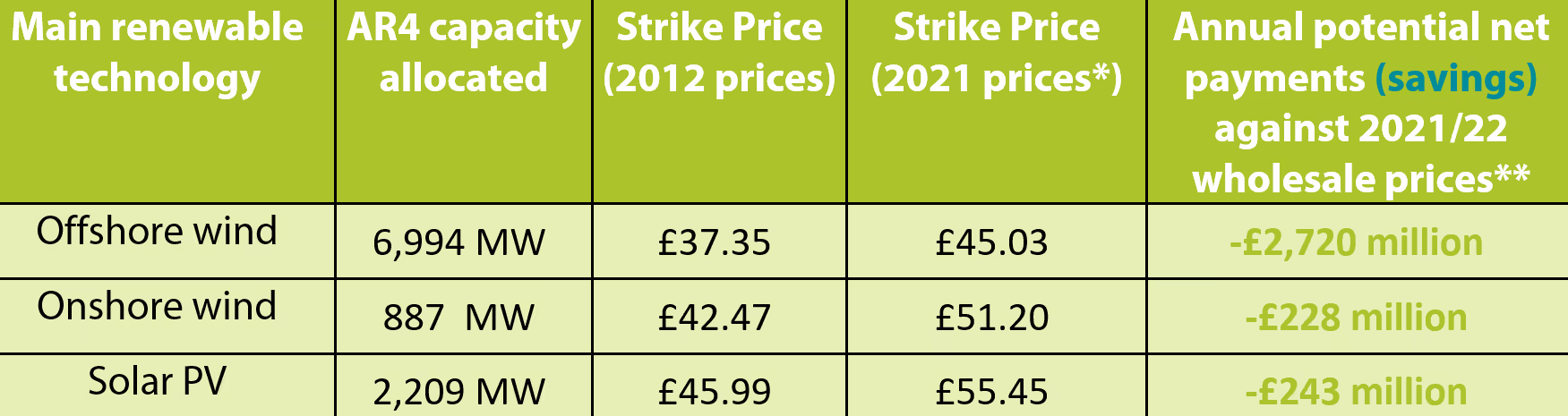

* Auction prices are expressed in 2012 prices; to convert to 2021 an inflation factor of 1.2056 has been usedÂ

** Using wind and solar generation profiles and wholesale references prices from June 2021 to May 2022Â

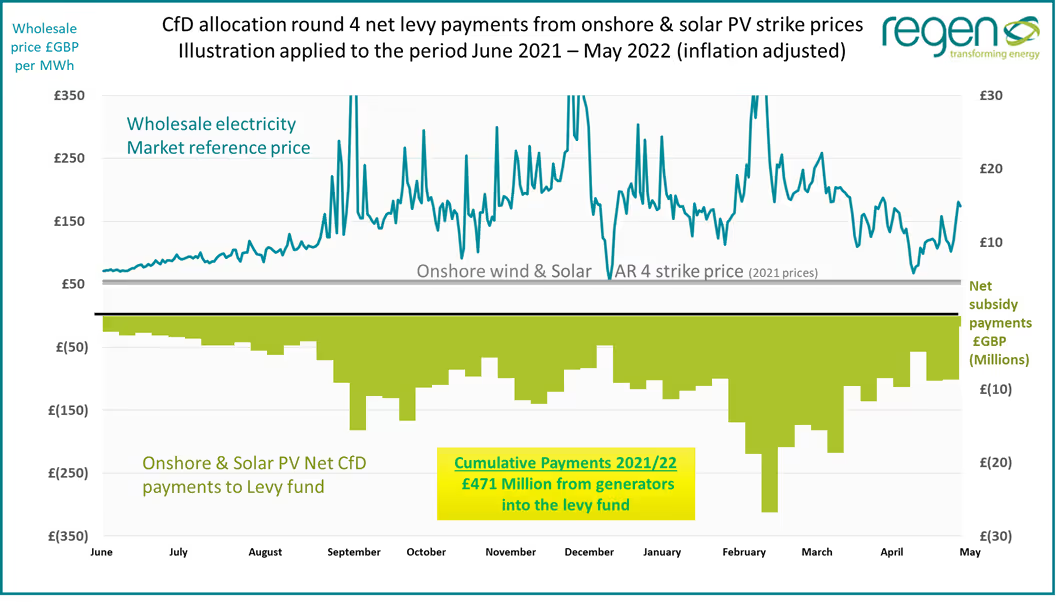

By our calculations, if the capacity of onshore wind and solar PV projects awarded contracts in AR4 had been built in June 2021, in time for the 2021/22 energy price crisis, they would have been making a significant contribution of over £471 million to reduce UK consumer bills in the last 12 months. That's an average saving of £64 per MWh compared to current wholesale prices. In blunt terms this is a direct opportunity cost of the Cameron government decision in 2016 to remove support from Pot 1 technologies in order to remove subsides from onshore wind.

Solar PV secured over 2 GW of capacity but the capacity of onshore wind, at 887 MW, could have been a lot more. Add in an earlier deployment of 7 GW of offshore wind at these prices, and the savings over the last 12 months would have topped £3.2 billion saving £99 per MWh generated.

Anyway, that's water under the bridge now, but we certainly hope that the next government recognises the consumer benefit that is being delivered by low cost renewables married with a CfD contract.

The low CfD prices demonstrate once again that renewable energy investors are willing to give up a significant amount of upside value, when prices are high, in order to obtain greater revenue certainty. This is a very important point that could form the basis of a new deal between generators and consumers; substantially lower consumer bills in exchange for lower investment risk.

Using this lever, the government could go much further as part of its Review of Energy Market Arrangement (REMA). As well as extending the use of CfDs for new generation capacity, a form of CfD could be offered, via auction, to existing generators including those who are currently holding legacy RO and FiT payments.

Going further still, the government could allow other participants to join the CfD scheme either as a direct counterparty to CfD contracts, or by selling the rights to CfD differential payments in a secondary market. The CfDs would still be underwritten by government, or one of its agents, but this would allow other energy buyers and consumers, in both the public and private sector, to effectively hedge their future energy supply at a very low cost. This is a better way to split the market for renewables and fossil fuels, rather than a Spanish style wholesale price cap as some have suggested.

Revenues made from selling CfD differential rights as a hedge could then be used to support fuel poverty and energy efficiency measures.

With over 7 GW at £37.35 per MWh, this was a massive auction round for offshore wind and a significant step towards meeting the government's 2030 target.

The bid price in AR4 has fallen again compared to AR3, albeit less dramatically than previous rounds. This is a very positive result which could easily have gone the other way. With increased wholesale prices, and increased commodity and supply chain costs for steel, copper, electrical components etc., CfD auction prices could well have risen in this round. Against this backdrop, the small price fall suggests that the offshore wind industry is continuing to make significant cost reductions through innovation and capability development.

It is great to see the first floating offshore wind project winning through in Cornwall, congratulations to the TwinHub team, and especially good to see the Wave Hub site finally begin to show its worth and enabling TwinHub to make a very low strike price bid of £87.30 per MWh for a 32 MW allocation.

Really we should have had a much bigger pot for floating wind and it would have been better to have at least two projects going forward. We would certainly like to see a much bigger and ringfenced allocation budget in AR5, albeit that, without the benefit of the Wave Hub infrastructure, floating wind strike prices may be higher in the next round.

Tidal is the other notable new entrant to obtain a first CfD. 28 MW of the 40 MW capacity awarded has gone to the next phase of the Meygen project in Pentland Firth, but congratulations also to the teams at Orbital and Magallanes Renovables who have also won contracts. At £178.54 per MWh, which was below the administrative price of £211, this was a very competitive auction and puts tidal energy on a better cost trajectory to become a viable technology for the future. Again we would like to see a further tidal stream ringfence and a bigger budget allocation in AR5.