Government to re-open Contracts for Difference for onshore wind and solar

BEIS has released a consultation on the Contracts for Difference (CfD) scheme that proposes bring back the ‘Pot 1’ auction for onshore wind and solar in the next auction in 2021. The deadline for responses is 22 May.

The proposals are a very positive signal that government policy on renewable power is shifting in response to the UK’s net-zero commitment. It is also good to see they have resuscitated the guidance that Regen wrote for government back in 2014 on best practice for wind projects on engaging with local communities. There are, however, plenty of issues for developers and investors to consider in a world where the government expects CfD bids below the wholesale price of power.

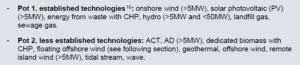

Pots and caps

The government has rejected the option of putting offshore wind into one technology neutral auction with solar and onshore wind, arguing that this could result in only a few of the lowest cost technologies being successful.

However, the consultation is also looking at separating offshore wind into a third pot, with the following two options proposed:

Option 1

Option 2

The consultation also proposes a separate definition and administrative strike price to bring forward floating offshore wind. The debate as to how fit for purpose CfDs are as a mechanism to support nascent technologies such as floating offshore wind from innovation stage to commercialisation will continue.

What is not clear is what caps there could be on each pot or across the auction as a whole. If there is a significant volume of Pot 1 auction bids below the wholesale price then the government is likely to want a capacity cap as well as a budget cap. The level this cap is set at is key – in the last auction round the cap for offshore wind was set at 6 GW.

Prices, public paybacks and investment strategies

The consultation makes clear the government expects Pot 1 auction bids below the wholesale price of power. Round 3 of the CfD auction cleared at £39.65 (2012 prices) for remote island onshore wind. Price competition between solar and wind, as well as within those technologies, seems likely to be fierce and developers and investors will need to think carefully about the value of the contracts vs forecast power prices and we may see some developers choosing to exit earlier in the process and leave CfD auctions to investors with large portfolios.

Planning and communities

Nothing in the proposals addresses the difficult planning environment for onshore wind in England which could mean proposals favour onshore wind in Scotland and Wales. There is a strong emphasis on working with local communities with a proposal to update the best practice guidance for onshore wind that DECC commissioned Regen to develop back in 2014 and a proposal for a register of community benefits, however focus is on best practice rather than mandatory considerations.

System integration

A new area for this round of CfDs is a focus on the overall system impact of CfD supported generation. The consultation is seeking views on the opportunities and challenges of storage co-locating with CfD sites. There is also a proposal to end payments for generators when prices are negative – potentially reducing the business case for storage at times of high generation.