Ofgem's consultation on how it intends to regulate gas networks during the RIIO-3 price control period raises questions about the future rise in gas network costs and eventual decommissioning, argues Frank Hodgson.

Ofgem's consultation on how it intends to regulate gas networks during the RIIO-3 price control period raises questions about the future rise in gas network costs and eventual decommissioning, argues Frank Hodgson.

Ofgem’s RIIO-3 sector-specific consultation raises important questions around how we prepare for the eventual decommissioning of the gas network and how we pay for the network through the transition.

In the week before Christmas Ofgem released its sector-specific consultation on how to manage the regulatory price controls for the gas transmission and distribution sectors during the RIIO-3 period. Buried in the Finance Annex lies some eye-opening analysis which raises important questions about how we transition fairly from gas to electricity. Although not a complete strategy, this annex shows that the regulator has begun to think about this difficult issue.

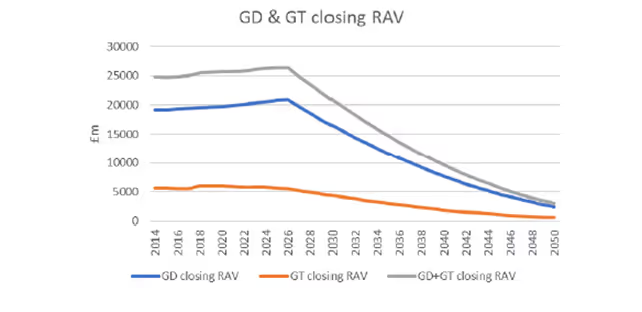

The key problem Ofgem has identified is how to pay for the £26.1 billion Regulated Asset Value (RAV) – the amount of outstanding capital value in network assets which has not been paid for by consumers – as households and industrial consumers disconnect from the gas networks. Without changes to the current approach consumers will face spiralling network charges and, despite increasing, not all costs will be covered by 2050.

Under the current regulatory model, network owners make investments in the energy networks which are then paid for by customer network charges to cover depreciation and a return on investment over the lifetimes of the assets. This approach, with depreciation over 45 years, will leave about £3bn of residual RAV in 2050 based on existing assets (see Figure 1). Any new investment during the ED3 period and beyond will increase the outstanding asset value and future network costs.

Ofgem points out that net zero in 2050 is incompatible with fossil gas assets having economic value beyond 2050 so it is considering reducing asset lives or ‘front-loading’ depreciation to accelerate the return on capital to asset owners.

The energy transition will have two major implications for gas networks:

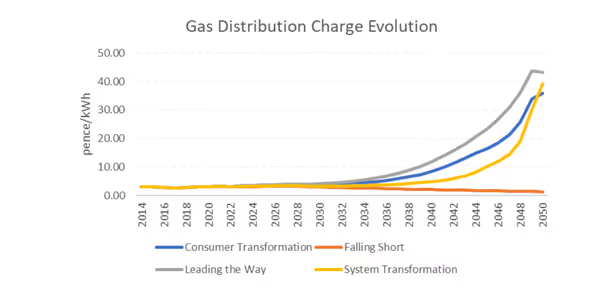

The impact of a falling customer base and lower gas consumption could see the energy unit cost of gas network charges rising rapidly from 2030 onwards.

Ofgem has estimated that network charges could reach 10p/kWh by 2040 and 40p/kWh by 2050. Network charges could accelerate earlier and end up higher if they include:

Increasing network charges would likely create a feedback loop as households and businesses will be incentivised to switch away from gas, raising network charges further. While many will see this as a positive and necessary step to drive the transition to net zero, the ramifications for those customers still using gas could be enormous.

Higher charges will raise the issue of fairness. Those consumers still using gas for heating in the late 2030s and into the 2040s may well be doing so because it is difficult for them to switch (such as those with lower incomes and the fuel poor, or people who cannot make the decision unilaterally like renters or people living in shared buildings of flats). Is it fair that those people pay for the remaining RAV balance while everyone else dashes to the exit? Ofgem is right to highlight the issue of fairness here.

In one area of good news for gas customers, Ofgem has clarified that hydrogen infrastructure development is out of scope for RIIO-3 and will be funded via the Hydrogen Transport Business Model (HTBM). Regen supports this, given that current users of natural gas (domestic, commercial and industrial) do not equate to future users of hydrogen (almost exclusively industrial) and will avoid consumers paying towards a fuel they don’t end up using.

Ofgem outlined five sources to plug the £3bn forecasted RAV gap:

None of these options are likely to be appealing to the Government or Ofgem.

The transition to net zero energy is going to have impacts on households across the UK, changing how we heat our homes and get about, the make-up of our bills and the jobs many of us do. Ensuring the transition is seen by households as fair and reasonable, that the benefits are enjoyed widely and the costs don’t fall disproportionately, is arguably biggest challenge we face – and a key focus for Regen.