As part of the delivery of the 2025 update to the Distribution Future Energy Scenarios (DFES), Regen has worked with the team at National Grid Electricity Distribution to publish research looking at the impact of data centres on distribution networks. This paper explores:

The current state of data centre development in the UK

Evolving data centre business models

The scale of new projects seeking grid connections

Some of the main locational factors driving the development of new sites, specifically those seeking to connect to the distribution network.

To inform this work, Regen interviewed data centre and property developers currently progressing new projects, to understand the main drivers, barriers and considerations for deciding where, when and how projects are scaled, sited and developed.

This paper also provides an analysis of the potential data centre capacity that could connect in NGED’s licence areas, as a new source of disruptive demand across the ED3 period and beyond.

Vantage data centre in Newport. Photograph: Colo-X

UK data centre development – a rapid rise of disruptive new demand connections

Data centres have become an increasingly hot topic for the energy sector, policymakers and wider society. Their development as large commercial buildings has been increasing since the 1990s, with the growth of the internet and online services. In recent years, the UK has also seen larger ‘hyperscale’ sites, serving a wider variety of services. With the increasing use of streaming services and the development of AI, further growth and increases in the scale of individual projects in the UK and worldwide are expected.

As part of the UK government’s AI Opportunities Action Plan, June 2025 saw the launch of a scheme to identify designated ‘AI Growth Zones'. These zones are intended to accelerate AI-enabled data centre development through streamlined spatial planning processes and enhanced access to large power supply connections and enabling infrastructure.

Data centre sites require a significant amount of power, and the volume of very large sites seeking grid connections with transmission and distribution network operators has increased significantly in recent years. With the UK government also identifying AI as a national economic growth opportunity, there is a need for energy network planning processes to assess the scale, timing and impact of a national, decentralised development of data centre projects.

NGED is already building this foresight into its long-term planning approach, integrating data centre growth scenarios into its system planning models to ensure capacity is ready where it’s needed most. By aligning with government growth zones and regional development priorities, NGED is helping to create the infrastructure foundation for the UK’s digital economy.

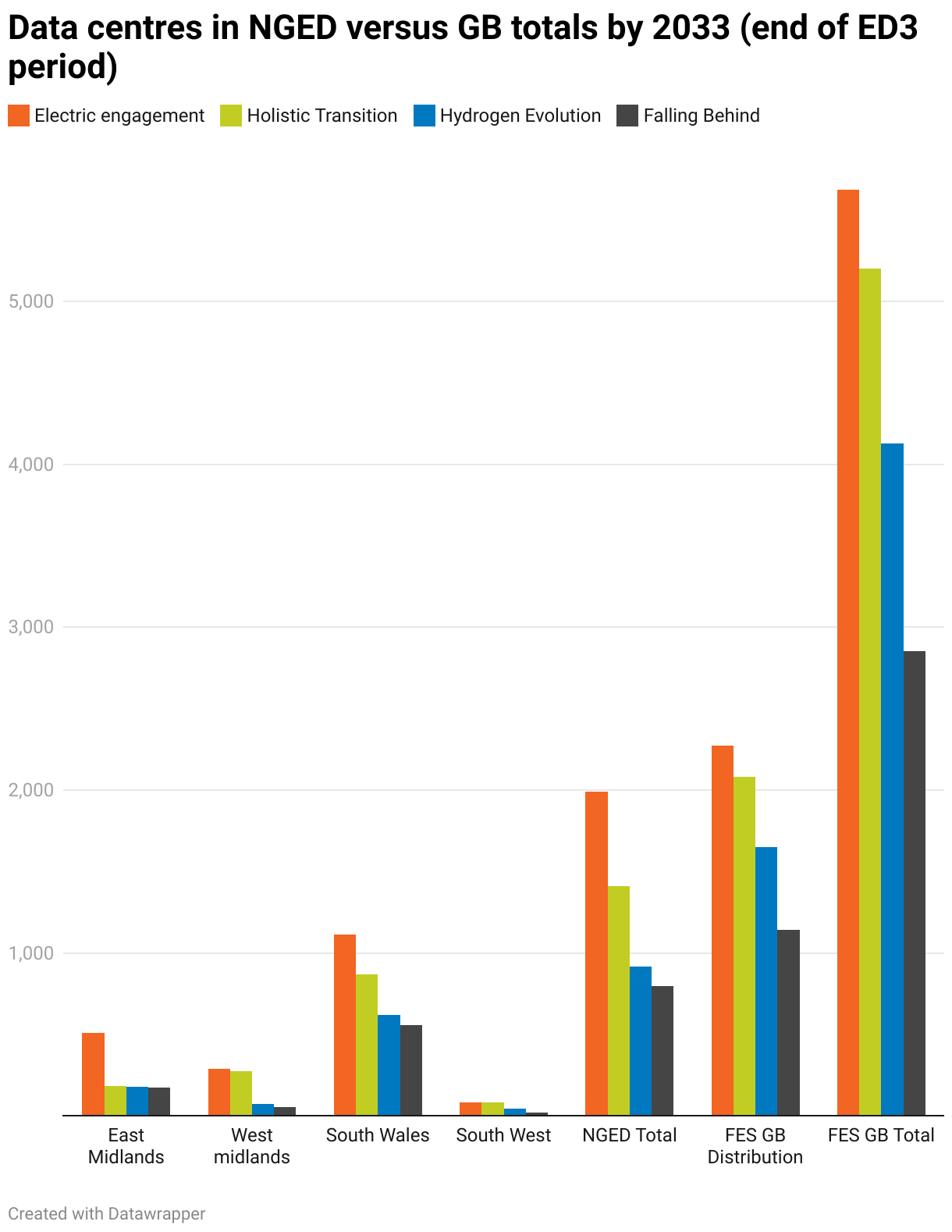

South Wales could be a hotspot for development

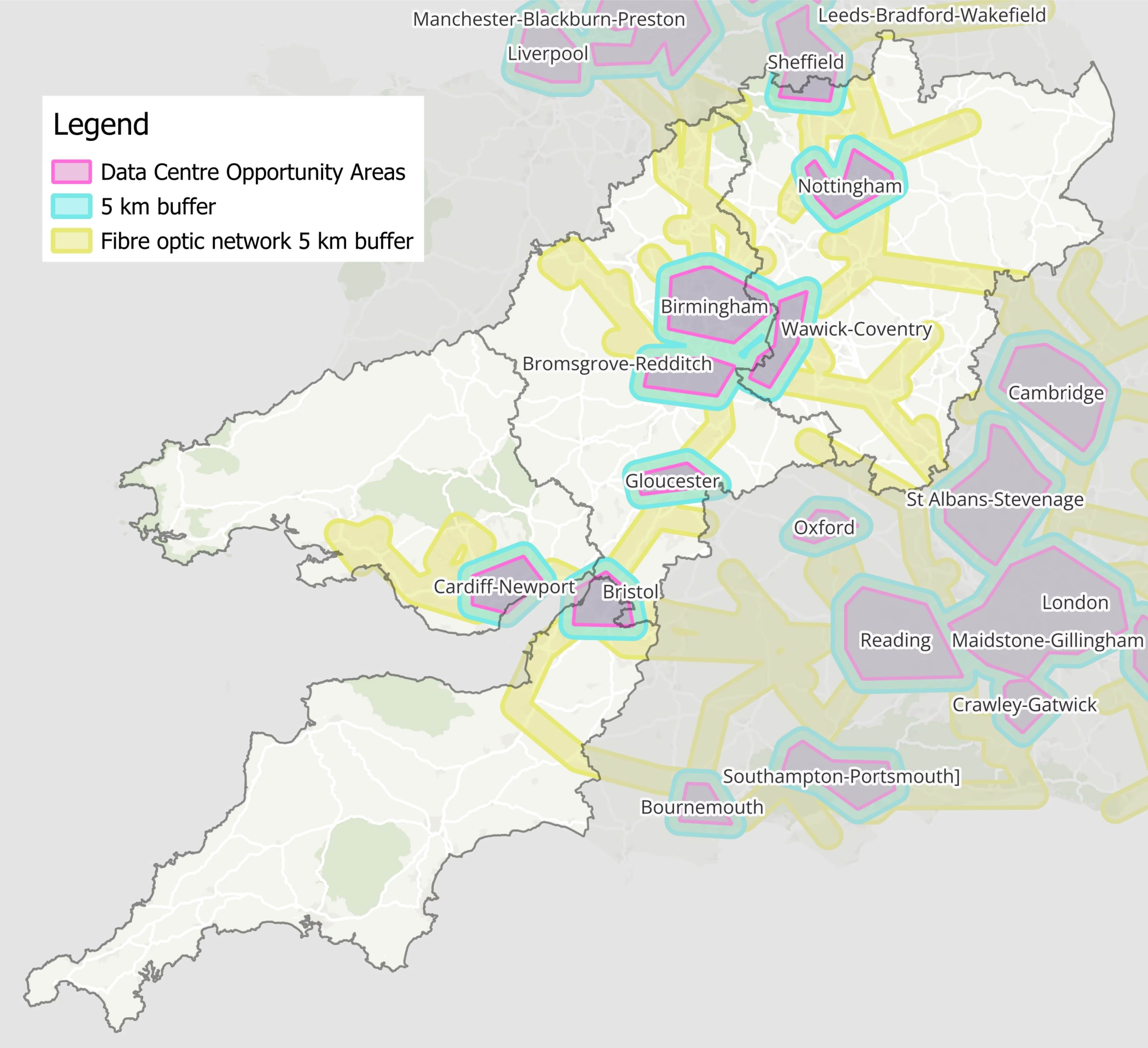

South Wales is set to be a potential hub for future data centre development, both on the transmission and distribution networks. Engagement with site developers, the announcement of Wales being identified to host at least one an AI Growth Zone and NGED’s pipeline evidence all points towards south Wales as being a licence area that could host significant data centre capacity.

Most of NGED’s pipeline capacity that is connecting in south Wales is targeting industrial areas outside of major population areas like Cardiff and Newport, where a fibre optic network infrastructure is also present.

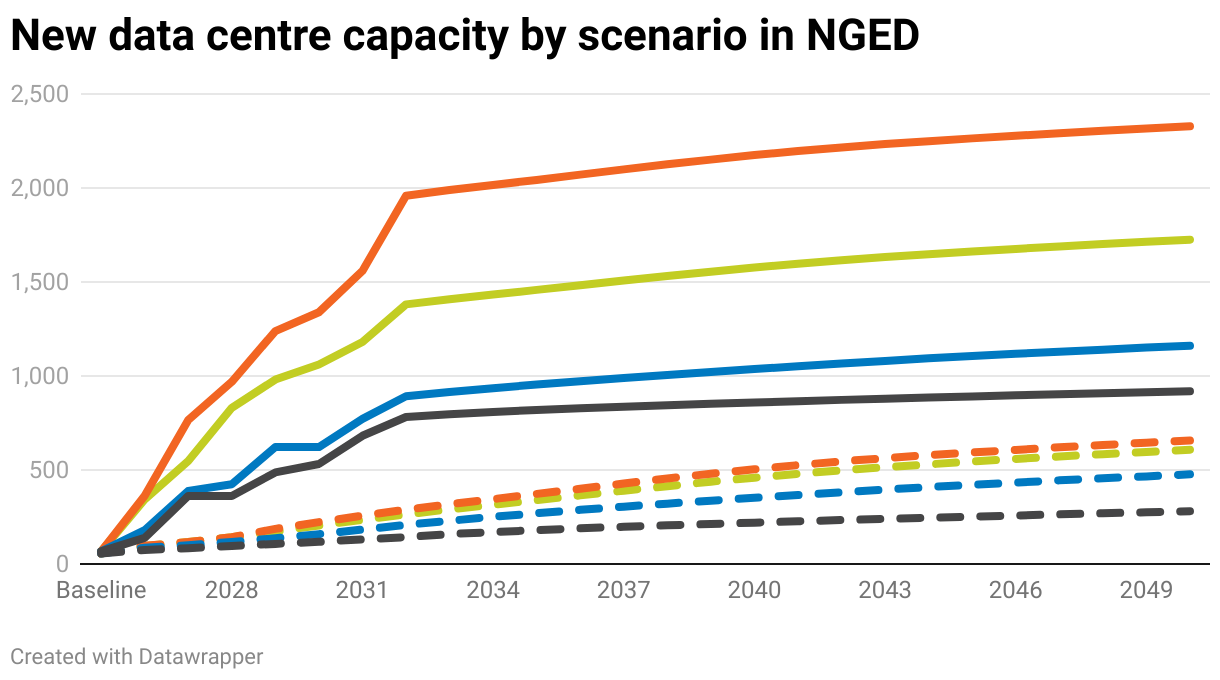

Our analysis shows that notable capacity could also connect across NGED’s licence areas, totalling c. 2 GW by the early 2030s under the most ambitious scenario.

The graphs above illustrate how pipeline capacity in NGED’s licence areas far exceeds the expected total projected capacity. For the purposes of comparison, Regen has used assumptions to estimate approximate FES distributed capacity projections based on assumptions applied to FES total GWh projections.

Data centre business models and project types are evolving

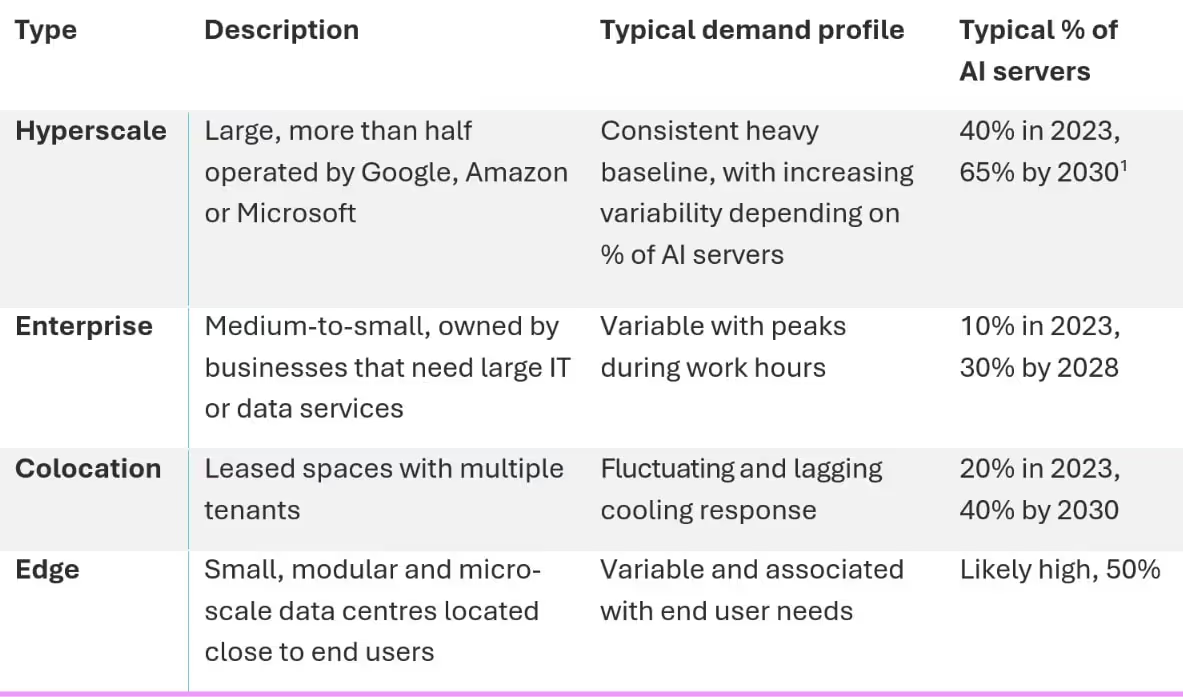

Data centres can be developed at varying scales; they can be standalone or colocated with other commercial premises and businesses. The growth of AI services and online tools is causing data centre business models and archetypes to change.

Table 1: Characteristics of data centre archetypes

An assessment of NGED’s demand connections data has revealed that, while a number of enterprise and small-scale colocation data centres are currently connected today, new data centres seeking grid connections are increasing significantly in scale. A surge of very large hyperscale sites are seen to be connecting, though it is unclear if some of these will remain distribution connected or look to move up to transmission network connections, if capacity becomes available at higher voltage tiers.

The proportion of AI servers housed in data centres will also have an impact on network connections. Data centres that host clients using IT infrastructure for AI inference will have more varied demand profiles compared to a traditional cloud business model, which is typically more stable and predictable.

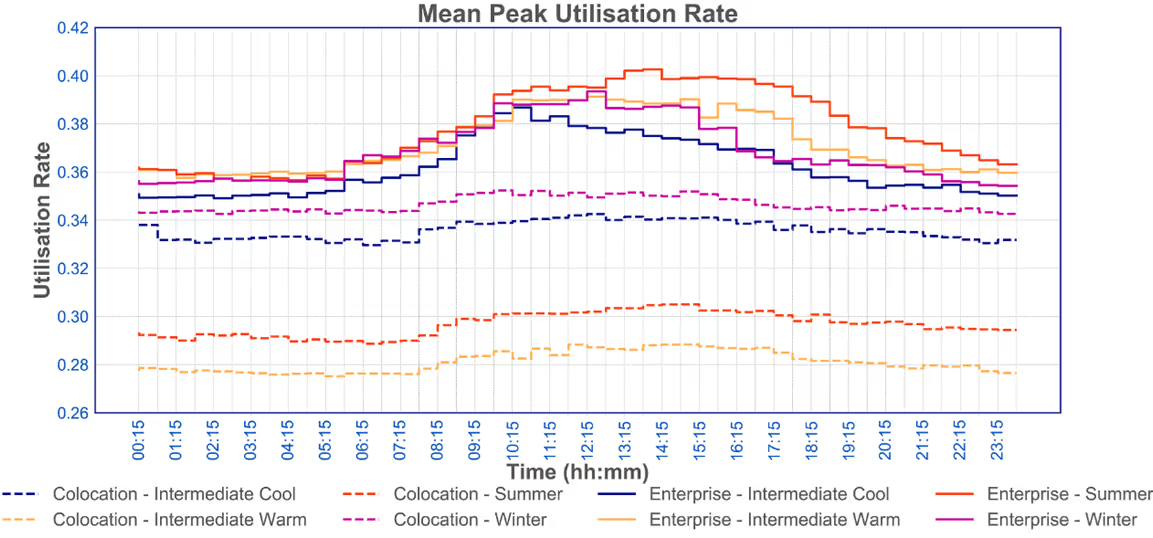

Load profiles

To understand the impact of future data centres on the distribution network, load profiles were created using measured data from existing data centres connected to NGED’s network to model their expected behaviour.

The results of this analysis will be used to plan the distribution network for edge-case peaks in load caused by future data centres in conjunction with other distribution connected technologies. Currently, NGED does not have measured data for hyperscale data centres, but multiple are due to connect. As more data becomes available, future iterations of load profile analysis will be undertaken to enhance understanding, particularly as hyperscale sites typically host the greatest density of AI server racks which display irregular load peaks.

The main factors driving the location of new data centres

There are a number of studies that have looked into the geographical factors that influence data centre developer decision making when identifying land for future sites. The availability of grid capacity remains a top priority, especially with the increasing size of hyperscale sites and server density. Engagement with data centre developers also identified the need to be in close proximity to end users (including large population centres), to avoid low latency of services. Developers are also concerned with access and proximity to fibre-optic networks. Other factors such as water availability, land availability and access to skilled workforce will all be considered in parallel.

Different types of data centres will be concerned with different locational factors. For instance, the emerging ‘edge’ business model is much more likely to be sited near areas of high population density, whereas hyperscale and enterprise data centres are likely to be more concerned with proximity to grid capacity and fibre-optic network infrastructure.

Through early engagement with data centre developers and regional partners, NGED is working to ensure that connections can be delivered efficiently, without compromising network resilience or decarbonisation goals.

Data centre opportunity areas in NGED's licence areas

How many data centres could we see across the UK?

The development of new data centres and the evolving nature of their business models, AI services and locational factors reinforce the need for electricity networks to understand the potential impact of this surge of site development.

With the UK government identifying AI as an economic opportunity for the country, the development of data centre projects, especially through the implementation of AI Growth Zones, could see rapid progress and some very large projects could be fast-tracked through planning.

Across the UK there is an increasing pipeline of prospective data centre projects seeking to connect at both transmission and distribution that could be into 10s of GWs.

How much capacity will be needed and at what levels is not yet fully understood, but with some developers seeking alternative solutions or sources of power to enable sites to operate in the near term, the development of data centres will continue to be a significant aspect of network load forecasting, including for the upcoming RIIO-ED3 regulatory period from 2028 to 2033.

“As the scale and pace of data centre development accelerates, our role is to anticipate, not just accommodate, this new wave of demand. By planning proactively and collaborating across the energy system, we can balance this rapid digital expansion with the long-term resilience and decarbonisation of our energy networks.” Oli Spink, head of system planning, National Grid Electricity Distribution

Regen's work on large electricity demand modelling

We continue to develop our expertise around data and digitalisation and the modelling of industrial electrification and large sources of disruptive demand. Our analysis of the data centre sector builds on methodologies we’ve developed to consider the electrification of rail, maritime, agriculture and airports for NGED, as well as understanding the potential electrification needs of industrial clusters.

As an organisation, we recognise that industrial electrification and industrial-scale electricity demand will continue to be a key consideration for clean power and net zero. Like many other organisations, Regen is looking to understand and explore the best use cases of AI in the energy industry. We are also very interested in getting into the detail of the question of its impact on energy networks and reaching our net zero goals. Data centres as sources of disruptive demand and the opportunities to understand or reduce energy system impact are key topics of interest moving forwards. If you are interested in engaging with Regen further in this space, please contact Tamsyn Lonsdale-Smith.