In a new report for Scottish Futures Trust, Regen associate Simon Gill argues that the ongoing Review of Electricity Market Arrangements is crucial to ensure Scotland can hit its decarbonisation targets and, by extension, to ensure that Great Britain can deliver a net zero electricity system by 2035.

Scotland has long aimed to lead when it comes to decarbonisation. It plans to reach net zero by 2045, while delivering a just transition and eradicating fuel poverty by 2040. But the size of its renewable resources means that Scotland also has a critical role to play beyond its own borders, supporting decarbonisation across the whole of Great Britain.

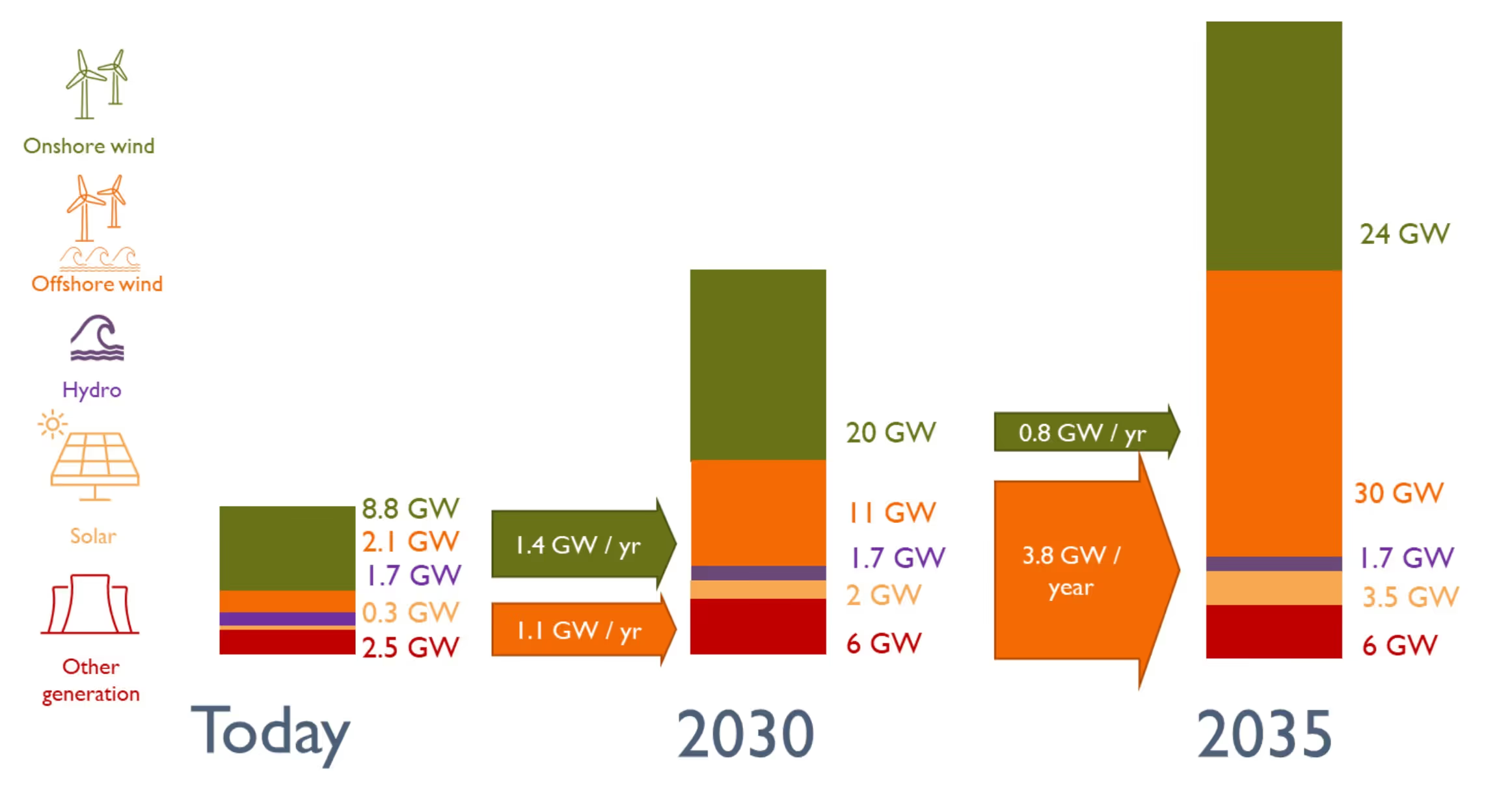

Scotland is home to around 10% of the British population, but its wet and windy climate means that more than a quarter of the British renewable generation fleet is found here –around 14 GW. Over the next decade, that capacity will need to grow quicker than in any other region of the country. All of the National Grid ESO's net zero compliant Future Energy Scenarios (FES) include at least 50 GW of renewable capacity hosted in Scotland by 2035. The implication is that, to meet the UK government's commitment to a zero carbon electricity system, Scotland needs to succeed in delivering much of the 28 GW of Scotwind offshore wind capacity, and exceed its target of 20 GW of onshore wind by 2030.

Figure 1: Illustrative pathway for Scottish generation capacity out to 2035 consistent with Scotland's declared ambitions in 2030, NGESO's net zero FES scenarios for 2035, and the Scottish whole energy system scenarios. Source: Scottish Futures Trust

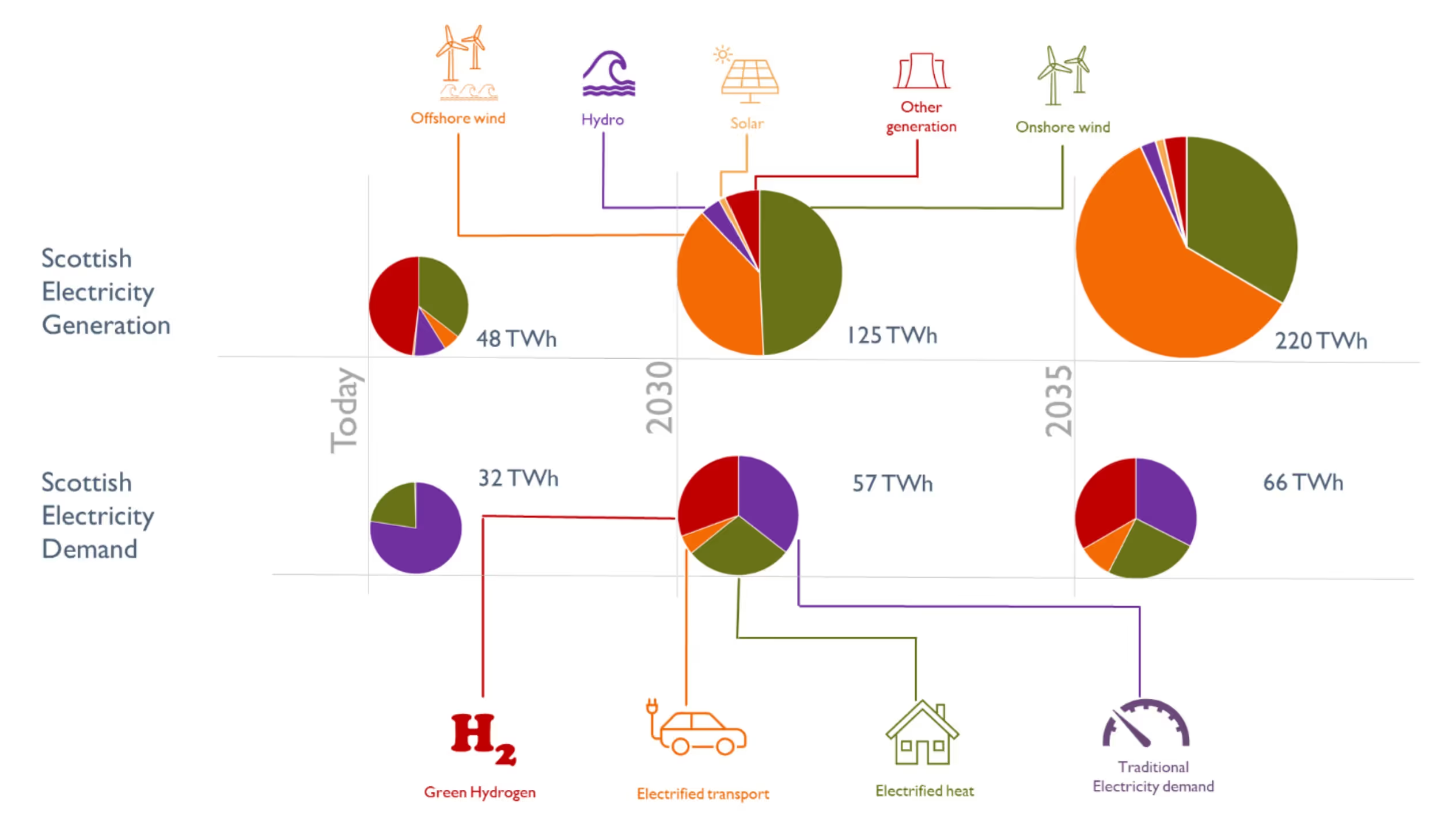

Figure 2: Illustration of annual electricity generation and demand in Scotland out to 2035. Values for today are based on current statistics, 2030 values are consistent with Scotland's declared ambitions (e.g. for the level of heat decarbonisation) and 2035 is broadly consistent with FES 2022 and the Scottish whole energy system scenarios. Source: Scottish Futures Trust

Scotland's draft energy strategy and just transition plan is built upon successfully delivering renewables, not just in terms of energy generated, which will significantly exceed Scotland's own demand, but also in terms of the impact on wider societal outcomes such as jobs, economic activity and community benefit. For example, low carbon jobs need to replace those lost through the decline of the oil and gas sector. The energy strategy and just transition plan states an expectation that Scottish low carbon jobs will rise from 19,000 today to 77,000 in 2050, and this is increasingly factored into wider societal planning across finance strategies and economic development.

The Review of Electricity Market Arrangements (REMA)

The significance of renewables means that Scotland is particularly exposed to changes in the way in which electricity markets are organised. In 2022 the UK government kicked off its detailed REMA process of reform, with the scope to make sweeping changes to wholesale market frameworks. Regen has argued since the start of REMA that GB needs a 'radical evolution' of market arrangements, based around a national bilaterally traded market, and supported by stronger strategic planning of the energy system. While this is important for GB overall, it is even more so for Scotland. The past decade has seen transmission reinforcement fall behind the growth of renewables, leading to high levels of network constraints and ultimately the need to curtail wind generation in Scotland. One of the major factors leading to the delay in transmission reinforcement has been regulatory frameworks that tended to take a risk-averse approach, considering individual network projects in isolation rather than as part of a wider portfolio designed to support a strategic system-wide outcome.

The high level of network constraints means Scotland will be more exposed than other areas of GB to major negative impacts of one of the main reform options under consideration: a move to locational marginal pricing (LMP). While we expect that nodal pricing, the most extreme form of LMP, is unlikely to feature strongly in the next REMA consultation from the UK government, we do expect zonal pricing to be one of the lead options.

What is LMP?

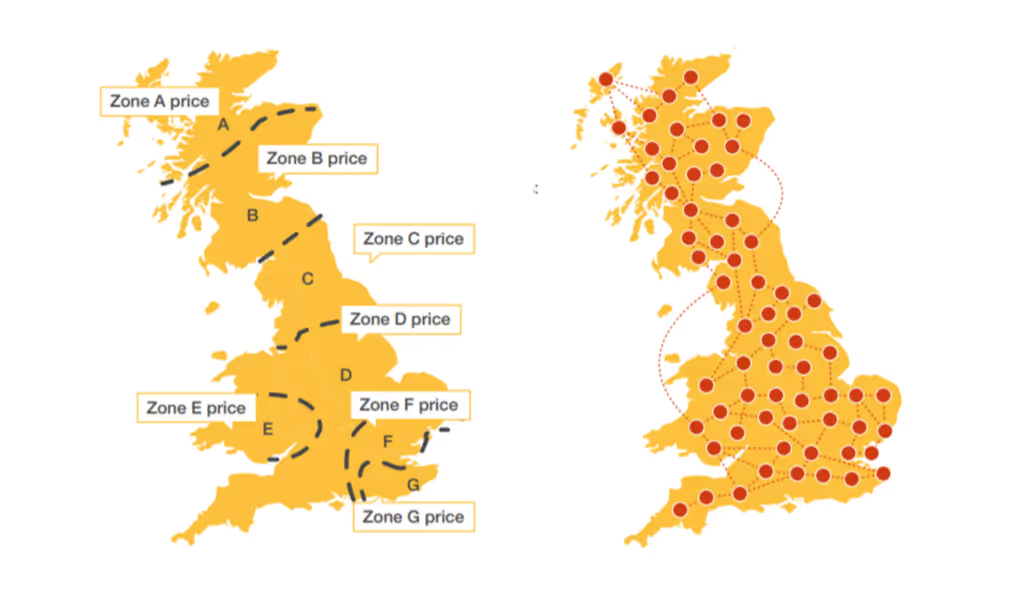

In simple terms, a shift to an LMP-based wholesale power market would see GB split into a series of zones or nodes, as illustrated in Figure 3, with electricity priced differently in each, to reflect the level of congestion and the incremental cost of meeting demand at each location. This would be coupled with a shift to a centralised dispatch process, where centrally managed optimisation tools are used to determine 'cost optimal' dispatch of generator outputs and settings of flexible demand and storage, based on bids and offers submitted by market participants to the system operator.

This represents a significant shift from the current system which is more decentralised, with electricity producers striking deals through bilateral forward contracts, Power Purchase Agreements, or trading on independent power exchanges, before notifying the system operator of their intention to generate.

Figure 3: Scottish generation and demand. Source: National Grid ESO

Regen recently wrote to the UK government making the point that neither zonal or nodal LMP would be beneficial to the GB energy system, either today or for the foreseeable future. The letter highlighted increased investment and development risk as factors that could derail net zero. Those concerns would be felt most acutely in Scotland, where zonal pricing would likely lead to a major drop in revenues, and the introduction of significant uncertainty for investors.

There will still be challenges for Scotland under other reform options. However, under options which build upon existing market arrangements, rather than instigating a completely new market framework, there is likely to be more opportunity to mitigate risk and develop an environment that delivers for consumers, encourages flexibility to support efficient operation of the system and maintains confidence for investors.

As an example of an evolutionary approach, Regen recently explored ways in which locational signals could be improved. We concluded that there are opportunities to deliver much more effective locational signals compared with today through strategic planning, reformed transmission charging arrangements, and improvements to the Balancing Mechanism.

A vision for market reform

The new Scottish Futures Trust report lays out a vision for market reform that is rooted in this evolutionary approach.

It argues that an evolution of the current national bilateral wholesale market is more suited to delivery of Scottish energy ambitions, including targets for renewables, and those focused on delivering for people and places. It acknowledges the challenge that we now face: market structures have failed to protect consumers against eyewatering price rises, the need to significantly increase the rate at which we build infrastructure, and the growing challenge of ensuring that energy is affordable for everyone in society for decades to come.

One point that the vision makes is that there is a need to better understand what people, as both consumers and citizens, want from the energy system. This means asking people how they see the balance and interaction between different outcomes: keeping bills down today, having confidence over the cost of energy in the future, and delivering positive environmental, societal and economic impacts.

In summary, based on the three principles put forward in the vision, delivering good outcomes from market reform for Scotland and for GB as a whole needs:

Coordinationbetween Scottish and UK/GB institutions, reflecting the fact that Scottish generation is needed to power much of GB in the next decade.

Commitment from all parties to make this work for consumers, both in the short term (low prices today) and the long term (stable prices in the future, good low carbon jobs, support for a strong economy, and meaningful contributions to community wealth).

Confidence for investors to ensure that the sector can deliver the investment in renewables and flexibility that society requires.

The report aims to support an informed debate, not just within Scotland, but about the role that different parts of the country have in supporting GB and UK national outcomes, and can be viewed in full here.