Following the announcement in December that the Viking Link interconnector has begun commercial operation, Ellie Brundrett provides an update on GB's current interconnector pipeline.

Following the announcement in December that the Viking Link interconnector has begun commercial operation, Ellie Brundrett provides an update on GB's current interconnector pipeline.

Interconnectors are expected to play a significant role in a net zero electricity system, both by providing a means of exporting renewable capacity and by supporting security of supply, by helping to meet peak winter demand on days when the wind isn’t blowing.

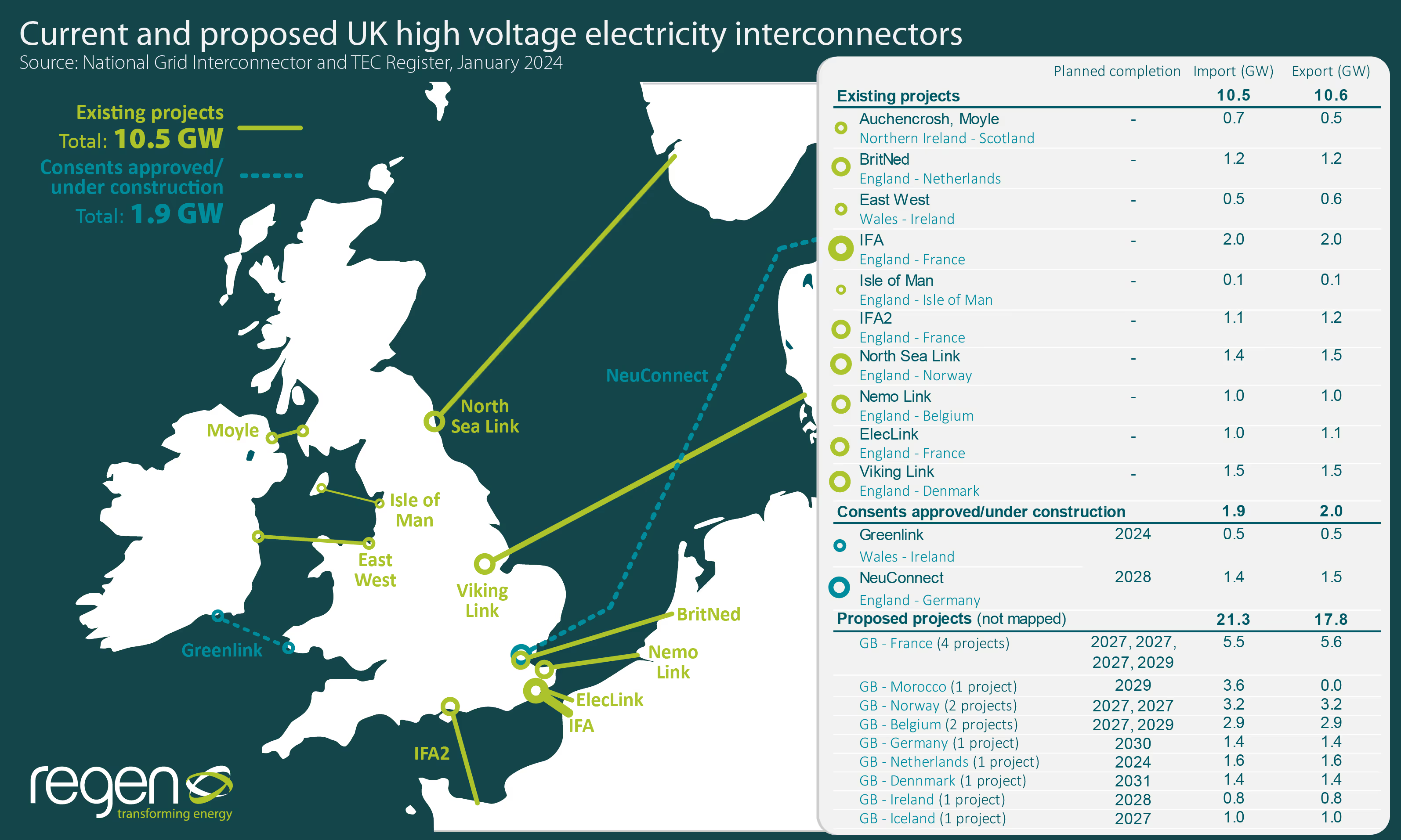

Since we last published this graphic in 2021, GB’s interconnector capacity has increased by 2.5 GW to 10.5 GW, with ElecLink to France coming online in 2022 and the Viking Link to Denmark coming online in 2023. This growth is expected to continue – the current pipeline of projects could see interconnector capacity exceed 20 GW by 2035.

While interconnectors are, in the physical sense, network assets, they are networks that connect two different markets, with each national market viewing the interconnector as either a producer or consumer of electricity. The European target model for electricity markets aims to use interconnectors to integrate different markets, but the UK’s exit from the EU and the Internal Energy Market complicates the picture for GB interconnectors.

Interconnector reform could explore a range of options to ensure that they are working in the best interests of the wider electricity system. This could include a more strategic approach to planning, such as including interconnectors in future iterations of Holistic Network Design (HND) creation, and market reform, such allowing interconnectors to participate in the Balancing Mechanism (BM) and increasing the ESO’s ability to adjust interconnector capacity or countertrade flows outside of the BM.